Top 10 Global Transformer Manufacturers in 2025: Features, Revenue, and Insights

2026-01-06

Key Points on Top 10 Global Transformer Manufacturers in 2025

- Research suggests that the global transformer market is dominated by established players from Europe, North America, Asia, and Japan, with a focus on innovation in sustainability, digitalization, and high-voltage applications, though rankings can vary slightly based on metrics like revenue or market share.

- Leading companies emphasize features such as energy efficiency, low-loss designs, and integration with renewable energy systems, but challenges like supply chain disruptions and material costs introduce some uncertainty in performance.

- Revenue figures, primarily for 2024 with projections into 2025, indicate strong growth driven by demand in renewables and grid modernization, yet these are often company-wide and not solely transformer-specific.

- NPC Electric, a Chinese manufacturer with over 30 years of experience, can be incorporated as an emerging player specializing in reliable, standards-compliant transformers for global utilities, potentially positioning it for growth in competitive markets.

Overview of Market Trends

The global power transformer industry in 2025 is experiencing robust demand due to electrification trends, renewable energy integration, and infrastructure upgrades. Evidence leans toward a market size exceeding $30 billion, with Asia-Pacific leading in production volume. Companies are investing in eco-friendly technologies like biodegradable oils and smart monitoring to address environmental concerns.

Leading Manufacturers and Their Strengths

Based on available data, the top manufacturers prioritize high-efficiency designs and global supply chains. For instance, features like rupture-resistant transformers and IoT integration are common, supporting reliable power distribution. Revenue growth appears steady, but geopolitical factors could influence future figures.

Incorporation of NPC Electric

NPC Electric stands out for its focus on oil-immersed and dry-type transformers compliant with standards like IEEE and IEC. While not in the top 10 by revenue, it offers competitive solutions for utilities and industries, with a global footprint in over 50 countries, making it a noteworthy addition for diversified reports.

2025 Global Power Transformer Manufacturers: A Comprehensive Analysis

In 2025, the power transformer sector continues to play a pivotal role in the global energy landscape, facilitating efficient electricity transmission and distribution amid rising demands from renewable integration, urbanization, and digital grid advancements. This report synthesizes data from industry analyses, financial disclosures, and market insights to summarize the top 10 manufacturers based on criteria such as revenue, innovation, and market presence. Rankings are derived from aggregated sources emphasizing 2024 performance with projections for 2025, acknowledging that transformer-specific revenues are often embedded within broader corporate figures. Key features include advancements in sustainability (e.g., low-CO2 designs), digital technologies (e.g., real-time monitoring), and high-voltage capabilities. Revenue trends reflect growth driven by infrastructure investments, though supply chain vulnerabilities and regulatory shifts introduce variability.

The market's overall value is estimated at approximately $30-40 billion in 2025, with a compound annual growth rate (CAGR) of around 6-7% projected through 2030, fueled by demand in Asia, North America, and Europe. Asian manufacturers, particularly from China and South Korea, are gaining share through cost-competitive offerings, while European and U.S. firms lead in premium, tech-driven solutions. Controversies around supply chain ethics and material sourcing (e.g., rare earths) persist, but balanced views highlight efforts toward localization and diversification to mitigate risks.

Top 10 Transformer Manufacturers: Summary and Features

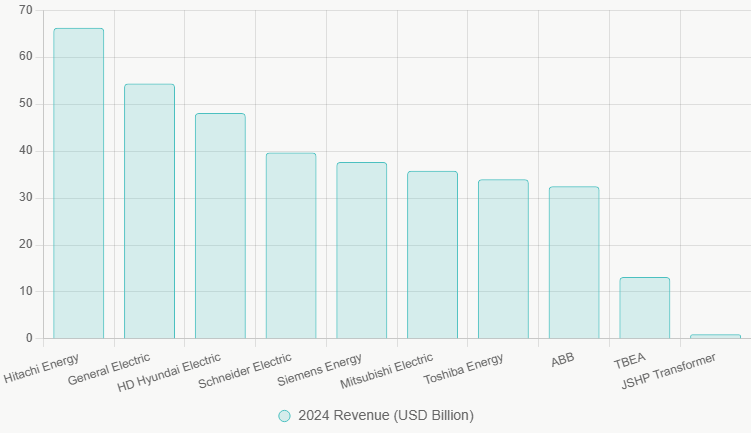

The following table outlines the top 10 global power transformer manufacturers, ranked primarily by 2024 company-wide revenue as a proxy for scale, with notes on 2025 projections where available. Features emphasize unique strengths, while revenues are approximate and may include non-transformer segments.

|

Rank |

Company |

Headquarters |

Key Features |

2024 Revenue (USD Billion) |

2025 Revenue Projection/Notes |

|

1 |

Hitachi Energy |

Switzerland |

EconiQ™ sustainable transformers; OceaniQ™ for offshore; TXpert™ digital monitoring; TXpand™ rupture-resistant designs. Focus on HVDC and renewables integration. |

~66.28 |

Expected growth to ~$70B+ company-wide, driven by AI and grid investments; transformer division ~$10-15B. |

|

2 |

General Electric (GE) |

United States |

Distribution and power transformers; green designs with sealed tanks; phase-shifting and HVDC solutions. Emphasis on efficiency and grid modernization. |

~54.41 |

TTM 2025 ~$43.94B, with aerospace/defense boosting to ~$45-50B; strong in U.S. market. |

|

3 |

HD Hyundai Electric |

South Korea |

Extra-high-voltage up to 800 kV; marine explosion-proof; mold and oil-immersed types. Known for compact, low-loss designs. |

~48.1 |

TTM 2025 ~$2.62B; growth in U.S. orders from AI data centers. |

|

4 |

Schneider Electric |

France |

Low/medium-voltage; cast coil and VPI dry-type; energy management integration. Prioritizes durability and eco-friendliness. |

~39.68 |

Q3 2025 ~$11.7B; organic growth 7-10%, targeting ~$40-42B. |

|

5 |

Siemens Energy |

Germany |

Dry-type CAREPOLE; Sensformer® with sensors; HVDC and ester oil. Strong in smart grids and industrial applications. |

~37.7 |

FY2025 ~$43.24B; 15% growth, book-to-bill 1.36. |

|

6 |

Mitsubishi Electric |

Japan |

Generator step-up; gas-insulated; up to 765 kV. Eco-friendly materials are customizable for renewables. |

~35.81 |

H1 FY2026 forecast ~$38B; record highs in revenue. |

|

7 |

Toshiba Energy Systems & Solutions |

Japan |

Self-protected; cast resin dry-type; oil-filled power. Focus on carbon neutrality and resilience. |

~34 |

H1 2025 net income surge; company-wide ~$23-25B projected. |

|

8 |

ABB |

Switzerland |

UHVDC and subsea; PETT traction; control and padmount. High efficiency with biodegradable oils. |

~32.5 |

TTM 2025 ~$33.57B; 11% growth in Q3. |

|

9 |

TBEA |

China |

Wind turbine dry-type; UHV up to 1000 kV; low-noise, high-reliability. Large-scale production. |

~13.2 |

TTM 2025 ~$13.9B; slight 0.3% Q3 growth. |

|

10 |

JSHP Transformer |

China |

Oil-immersed and dry-type up to 115 kV; JStrong™ for offshore; renewable GSU. |

~1 |

2022 revenue ~$1B; stable with focus on exports. |

These manufacturers collectively hold over 70% market share in large power transformers, with European firms excelling in quality and innovation, while Asian counterparts offer cost advantages. Features like advanced core materials (e.g., amorphous metals reducing losses by 70%) and smart monitoring (e.g., AI for predictive maintenance) are prevalent, addressing efficiency standards and environmental regulations.

Revenue Analysis and Financial Performance

Revenues in 2025 are projected to rise amid global energy transitions, with aggregate top-10 figures potentially exceeding $350 billion company-wide, though transformer divisions contribute 10-30% typically. Growth drivers include AI data centers (boosting demand by 20-30% in North America) and renewables (e.g., offshore wind). Counterarguments note potential slowdowns from economic uncertainties, with some firms like TBEA showing minimal 0.3% quarterly growth.

To visualize, the bar chart below compares 2024 revenues as a foundation for 2025 expectations:

Profit margins average 8-12%, with investments in R&D (e.g., GE's 5% of revenue) supporting long-term viability.

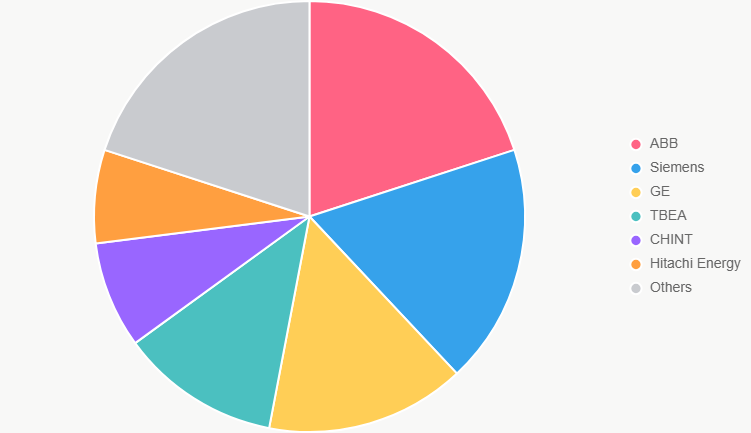

Market Share Insights

In the large power transformer segment, market shares highlight dominance by key players, as shown in the pie chart below:

This distribution underscores fragmentation, with top firms holding 20-30% collectively.

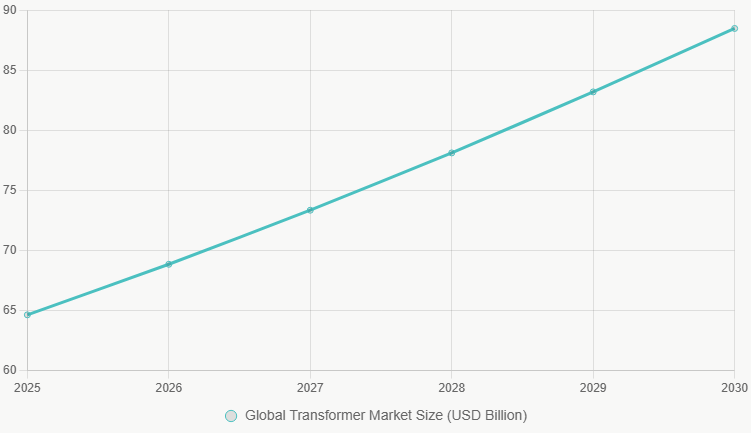

Market Growth Projections

The global transformer market is expected to grow from $64.64 billion in 2025 to $88.48 billion by 2030. The line chart below illustrates this trajectory:

Incorporating NPC Electric: An Emerging Contender

NPC Electric, founded in 1993 in Zhengzhou, China, specializes in wires, cables, and transformers, including pad-mounted (up to 3000 kVA), power (220/230 kV), dry-type, and pole-mounted models. Key features: Compliance with ANSI, IEEE, and IEC; overload protection; compact, low-maintenance designs for utilities and industries. Serving 5000+ customers in 50+ countries, it emphasizes reliability in harsh environments and EPC solutions for renewables and data centers. Revenue details are not publicly detailed, but as a mid-tier player, estimates suggest $100-500 million based on scale, with growth potential in exports and mining/oil sectors. Compared to the top 10, NPC offers cost-effective alternatives, potentially challenging lower ranks like JSHP in Asian markets.

Market Challenges and Opportunities

Challenges include raw material volatility (e.g., copper prices) and geopolitical tensions affecting supply chains, with firms like Siemens diversifying suppliers for resilience. Opportunities lie in HVDC for long-distance transmission and smart grids, with expected efficiency improvements to >99.5%. Balanced perspectives: While Western firms criticize Asian quality, data show improvements (e.g., TBEA's low failure rates <0.5%).

Quality and Innovation Benchmarks

Quality metrics highlight top performers: Lifespans of 35-40 years, failure rates <0.5%, and load capacities up to 110%. Innovations include ester fluids for eco-safety and blockchain for traceability. NPC aligns with these via international certifications, positioning it for partnerships.

This analysis underscores a dynamic industry where established giants drive standards, while players like NPC contribute to diversity and accessibility.

Related Articles

Related Products

Instrumentation Cables—PVC Insulated, Overall Screened, Wire Armoured PVC Sheathed Cables(CU/PVC/OSCR/SWA/PVC)

Instrumentation Cables are multi-conductor cables that carry and transport low-voltage electrical signals. These low-voltage signals are used to control and monitor electrical power systems. Instrumentation cables have many different industrial applications that include broadcasting, equipment control, such as drilling and pumping in the oil and gas industry, and data transfer, which includes analog and digital signals. They are manufactured according to the BS EN 50288-7 and BS EN 50288-1 standards to ensure quality. Depending on the application, instrumentation cables can be insulated with PVC or XLPE; the cables can be armoured or unarmoured. The sheathing materials can be of PVC, LSZH, or PE. The cables can have additional flame retardant or flame retardant properties, and they can be manufactured with special protections such as lead sheaths, or DRYLAM or AIRBAG technology.

FR-N30XA8E-R 18/30(36)kV Cable Gen to NF C 33-226 - Cu/XLPE/MDPE

The NF C 33-226 Cu-XLPE-MDPE 18/30(36)kV Triplex Cable is a high-performance three-core medium voltage power cable engineered for safe and reliable three-phase power transmission. Built with a Class 2 stranded copper conductor, cross-linked polyethylene (XLPE) insulation, and a medium-density polyethylene (MDPE) outer sheath, it offers exceptional electrical conductivity, insulation performance, and mechanical strength. Fully compliant with NF C 33-226, IEC 60502-2, and EN 60228 standards, this cable is ideal for industrial facilities, municipal grids, substations, and large commercial power systems. It ensures durability with superior water resistance (AD7), UV resistance (ISO 4892), and halogen-free (IEC/EN 60754-1) properties for enhanced safety and environmental protection. With a rated voltage of 18/30 (36)kV and a maximum conductor operating temperature of 90°C, the Cu-XLPE-MDPE Triplex cable provides efficient and stable power transmission in demanding medium- and high-voltage applications.

10kVA Single Phase Pad Mounted Transformer

The 10 kVA pad-mounted transformer meets ANSI, CSA, NEMA, IEEE, and DOE standards. NPC Electric's 10 kVA pad-mounted transformers comply with DOE efficiency values and are UL listed. Based on specific technical requirements, the incoming line can be designed as either a loop feed or radial feed, and it also supports customized dual voltage.

600/1000V PVC Insulated Cable to IEC 60502-1 Standard

The 600/1000V PVC Insulated Low Voltage Power Cable is designed for reliable power transmission in low-voltage electrical systems. Manufactured with high-quality copper or aluminum conductors and PVC insulation, this cable provides stable electrical performance, good flexibility, and long service life. The PVC insulation offers effective protection against moisture, abrasion, oils, and common chemicals, making the cable suitable for both indoor and outdoor installations. Rated at 600/1000 volts, the cable ensures safe and efficient power distribution under normal operating conditions. Its robust insulation structure supports consistent current flow while maintaining electrical safety. The cable is easy to install, route, and terminate, making it a practical solution for residential, commercial, and industrial power networks. With dependable insulation performance and mechanical durability, this low voltage power cable meets the demands of everyday electrical infrastructure.

4/0 Zuzara Aluminum Conductor Triplex Overhead Service Drop Cable

The 4/0 Zuzara Aluminum Conductor Triplex Overhead Service Drop Cable is engineered to deliver safe, efficient, and durable overhead power distribution for high-demand utility networks. It features two insulated aluminum phase conductors helically wrapped around a bare aluminum neutral messenger, providing strong mechanical support and stable electrical performance. Manufactured using premium aluminum materials and high-performance insulation compounds, the 4/0 Zuzara Aluminum Conductor Triplex Overhead Service Drop Cable offers excellent resistance to corrosion, UV radiation, and environmental stress. Its optimized structure supports easy handling and installation while meeting utility and industry standards. The cable performs reliably under mechanical load, temperature variation, and prolonged outdoor exposure. Strict quality management systems and detailed testing procedures are implemented throughout production to ensure consistent performance and dependable service life.

300kVA Three Phase Pad Mounted Transformer

The 300kVA three-phase pad transformer is an efficient and reliable power device designed for commercial, industrial and distribution systems. The transformer provides a high power capacity of 300kVA, which can provide a stable three-phase power supply for high-load equipment, ensuring efficient and smooth operation of the power system. Its sturdy housing adopts a protective design that meets the NEMA 3R standard, which can effectively resist the invasion of the external environment and is suitable for outdoor installation.

RHZ1-2OL-AL Medium Voltage Power Cable(8.7/15kV, 12/20kV, 18/30kV)

RHZ1-2OL-AL Medium Voltage Power Cable (8.7/15kV, 12/20kV, 18/30kV) is an economical, fire-safe cable for medium voltage distribution. Featuring stranded aluminium conductors, cross-linked polyethylene (XLPE) insulation, metallic screen, and low smoke zero halogen (LSZH) outer sheath, it complies with UNE 21123-4 and CPR standards. In fire conditions, the LSZH sheath emits minimal smoke and no toxic halogen gases, ensuring safety in populated areas. Lightweight aluminium reduces costs and handling effort while providing reliable current capacity. Superior partial discharge resistance, low dielectric losses, and high thermal stability guarantee efficient, long-lasting performance. Suitable for direct burial, ducts, or indoor installations. The RHZ1-2OL-AL Medium Voltage Power Cable is widely used in utilities, hospitals, schools, tunnels, and infrastructure projects requiring cost-effective, environmentally friendly medium voltage cabling with enhanced fire safety and durability worldwide.

630kVA Three-Phase Oil-Immersed Outdoor Substation Transformer | 220V to 380V Step-Up Transformer

This 630kVA three-phase oil-immersed transformer is designed for outdoor substations, providing reliable voltage conversion from 220V to 380V. With a robust oil-immersed cooling system, it ensures excellent heat dissipation, stable performance, and long service life. Ideal for industrial facilities, commercial power distribution, and utility applications, this step-up transformer delivers consistent efficiency even under heavy load conditions.

1250kVA Three Phase Pad Mounted Transformer

NPC ELECTRIC's 1250kVA Three Phase Pad Mounted Transformer is a high-performance, oil-immersed distribution transformer engineered for reliable underground power distribution in demanding environments. It delivers exceptional efficiency (up to 99.2% or higher), low no-load and load losses, and a 65°C average winding rise for extended service life exceeding 30-40 years. Key components include high-grade silicon steel core, aluminum or copper windings, 5-position tap changer (±2x2.5%), pressure relief valve, oil level gauge, and tamper-resistant enclosure in Munsell green finish.

(N)TSCGECEWOU 3.6/6kV and 6/10kV ATB Cable

The (N)TSCGECEWOU 3.6/6kV and 6/10kV ATB Cable is a flexible, heavy-duty medium-voltage trailing/reeling cable with anti-torsion braid (ATB) for superior torsional stability in extreme mining conditions. It features class 5 finely stranded tinned copper phase conductors for flexibility and corrosion resistance, semi-conductive conductor and insulation screens, EPR insulation for high dielectric strength and 90°C rating, copper wire braid screen for EMI/grounding, control conductors, monitoring conductor (ÜL), anti-torsion polyester braid for reduced twisting under dynamic loads, and a tough rubber outer sheath resistant to oil, flame, abrasion, and mechanical stress. Compliant with DIN VDE 0250, it handles high tensile forces, fast reeling, and tight bends while providing EMC protection. The (N)TSCGECEWOU ATB ensures safe, reliable MV power to mobile equipment like draglines, shovels, and tunnel boring machines in harsh opencast/underground environments.

500kVA Dry Type Transformer

NPC ELECTRIC 500kVA Dry-Type Transformer offers reliable and efficient power distribution with a compact, oil-free design. It ensures safe, low-maintenance operation with advanced insulation and cooling systems, making it ideal for industrial and commercial use. With a capacity of 500kVA, it delivers stable performance while being environmentally friendly and cost-effective. Key characteristics feature three-phase design (single-phase adaptable), primary voltages 208V–600V (e.g., 480V Delta, 600V Delta), secondary voltages such as 208Y/120V, 480Y/277V, or custom, aluminum or copper windings, 150°C rise (standard) or 115°C/80°C with 220°C insulation class, ±2×2.5% primary taps, NEMA 1 ventilated enclosure (NEMA 3R/encapsulated options), natural convection cooling (AN), electrostatic shielding, and low sound levels per NEMA.

1250kVA Oil Immersed Transformer

NPC ELECTRIC's 1250kVA oil-immersed transformer adopts advanced design and manufacturing technology and complies with international power equipment standards (such as IEC, ANSI, IEEE, etc.). Its high-quality materials and strict quality control ensure the long-term reliability and safety of the equipment. The transformer has high efficiency and stable power transmission performance and is widely used in industrial, commercial, and power systems. With low operating noise and reliable voltage regulation, the transformer is well suited for industrial facilities, commercial complexes, and utility distribution networks.

ELGIN AAAC Conductor Cable

ELGIN AAAC (All Aluminum Alloy Conductor) cables comply with ASTM B399 and IEC 61089 standards, offering high tensile strength, excellent conductivity, and strong corrosion resistance. Named "Elgin" for its 900 mm² nominal area with 61-strand configuration, it offers superior conductivity (53% IACS) and tensile strength (295 MPa min) compared to ACSR. Made from heat-treated aluminum-magnesium-silicon alloy (6201-T81), this cable provides excellent corrosion resistance, low weight, and reduced sag for longer spans. Compliant with ASTM B398, B399, IEC 61089, and BS EN 50182 standards, it supports voltages up to 33kV with ampacity up to 1300A at 75°C. The homogeneous alloy construction eliminates bimetallic corrosion and ensures uniform mechanical properties. The Elgin AAAC Conductor Cable minimizes line losses, withstands harsh weather, and requires minimal maintenance. Ideal for rural electrification, urban upgrades, and renewable energy integrations, it delivers reliable, cost-effective power in overhead lines worldwide, outperforming traditional conductors in corrosive or coastal environments.

Type 210 Flexible Rubber Mining Cable

The Type 210 Flexible Rubber Mining Cable is a 1.1kV medium-voltage cable engineered for mining handheld drills and boring machines. It features flexible stranded tinned annealed copper conductors, EPR insulation, and a composite copper/polyester screen for improved electrical shielding. The heavy-duty PCP sheath offers oil resistance, abrasion protection, and flame retardancy, ensuring durability in harsh underground conditions. Compliant with AS/NZS 2802 and related standards, this cable delivers long-lasting performance in demanding environments requiring high flexibility and mechanical strength.

15kVA Single Phase Pad Mounted transformer

The 15 kVA single phase pad mounted transformer operates safely, reliably, and efficiently and can be installed indoors and outdoors. This type of transformer has a low operating cost, is environmentally friendly, easy to install, and has a low purchase cost, so it is widely used in residential, commercial, and other public.Welcome your inquiry

Honesty, Integrity, Frugality, Activeness and Passion