Transformer Market 2025 Performance and 2026 Outlook

2026-01-04

The global transformer market experienced robust growth in 2025, driven by surging electricity demand, grid modernization, and renewable energy integration. In 2025, the global transformer market was valued at roughly $61.3 billion, with power and distribution transformers accounting for the largest shares. Key end-markets include utility transmission, industrial infrastructure, commercial buildings, and renewables (solar, wind, EV charging). Across all categories, manufacturers are expanding capacity to address a multi-year supply crunch. Notably, Wood Mackenzie reports that U.S. transformer demand has outpaced supply, with power-transformer demand up 119% since 2019 and distribution-transformer demand up 34%. Aging infrastructure (e.g., 40 million US distribution units beyond service life) and new loads (data centers, EV fleets) are key drivers.

Below we summarize 2025 market size (USD and, where available, units/MVA) and segmentation for four transformer types – pad‑mounted, power, dry‑type, and distribution – along with regional highlights (North America, South America, Europe), and 2026 forecasts. Competitive dynamics and leading manufacturers are noted for each category. Where available, key data are tabulated or graphed for clarity.

Pad‑Mounted Transformers

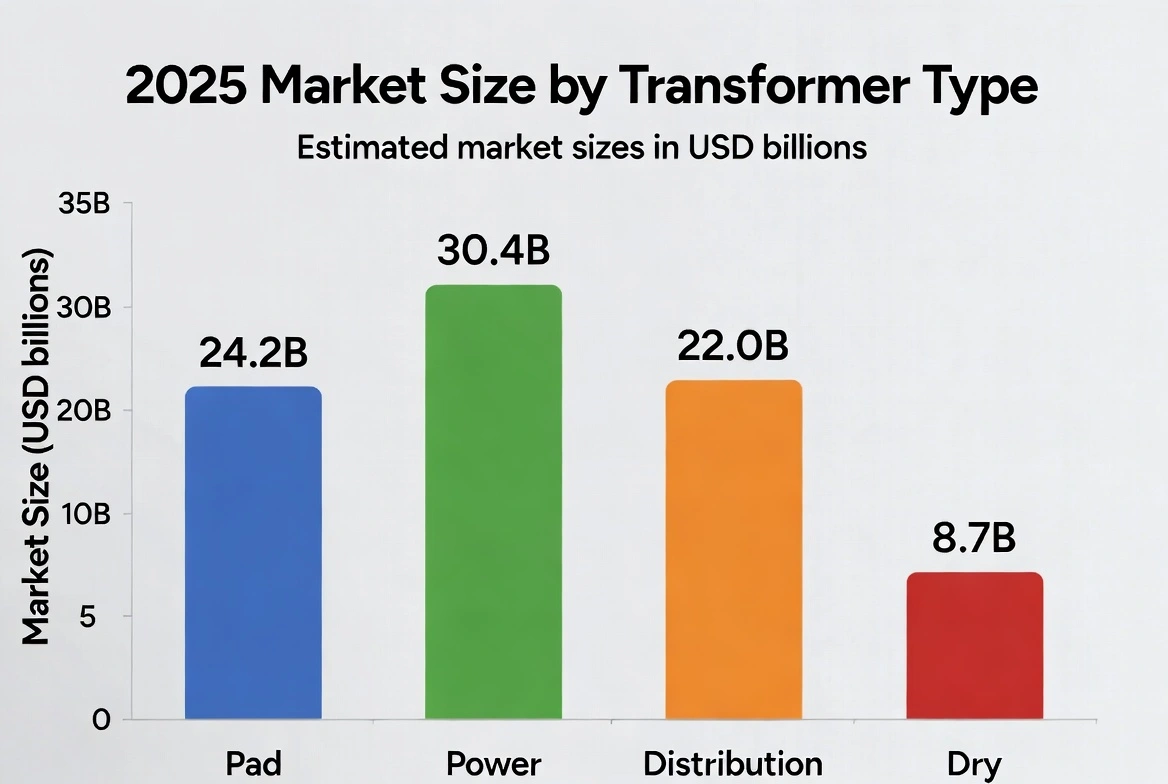

Pad‑mounted transformers (vaulted, ground-level units for distribution voltage) are widely used in residential, commercial, and light-industrial networks. They are built on concrete pads with tamper-resistant enclosures, making them ideal for urban/suburban power distribution, especially near homes, malls, and campuses. In 2025, the global pad‑mounted transformer market was about $24.15 billion. This follows a 2024 base of ~$22.3B (per Global Market Insights) and reflects growth of roughly 8–9%. North America and Europe both see strong pad‑mount demand: the U.S. is expanding distribution grids and adding renewable generation (solar/wind) in residential areas, and European countries (Germany, UK, Spain, Italy, etc.) are investing heavily in smart grids and rooftop solar, boosting pad‑mounted installation. Asia Pacific leads globally – China and India are rapidly urbanizing and electrifying, driving the largest share of new pad-mounted units – but detailed regional breakdowns for 2025 are not publicly reported.

2025 segmentation and drivers: Most pad transformers are three-phase units for multi-family or commercial blocks. In 2025, single-phase pad transformers (<1 MVA) dominated the residential segment. Key growth drivers include rising urbanization, grid expansion, and rooftop solar deployment. Fortune Business Insights notes that “adoption of rooftop solar PV in the residential sector” and massive utility T&D upgrades are boosting pad‑mount demand. However, competition from pole-mount solutions (which require no additional land) is a restraint. The pad‑mount market is also seasonally influenced by infrastructure stimulus; for example, U.S. utility contracts for pad-unit replacements were announced in 2024–25 (e.g,. Mohawk Valley Utility replacing several units).

Forecast (2026): Fort. Business Insights forecasts pad‑mount revenue to grow from $24.15B in 2025 to $25.77B in 2026, a CAGR of ~6.7% (2025–2034). We therefore expect ~6–7% growth in 2026, reaching roughly $26–27 billion globally. Growth will be driven by the same factors (solar build-out, grid refresh) and a chronic shortage of pad transformers in NA (WoodMac projects worsening shortages in 2026 due to data-center and EV charger loads). The new U.S. and Canadian manufacturing expansions (e.g., Hitachi Energy’s major investments) may start to ease lead times, but demand is expected to stay strong.

Competitive landscape: Major pad-mounted transformer manufacturers include ABB (Hitachi Energy), Schneider Electric, Eaton, Prolec GE, Siemens Energy, CG (General Electric), Sunbelt Transformer, Olsun Electric, Wenzhou Rockwell, Ermco, Pearl, and Hitachi America. These firms supply standard pad units as well as modular designs (e.g., factory-integrated switchgear). In 2025–2026, companies are expanding capacity (e.g,. Eaton’s $340M US investment for 3-phase pads) and innovating on smart-pad units (embedded sensors for monitoring). The market remains fragmented regionally, with local players (e.g., Transformers companies in Brazil and Asia) also present.

| Category | Global Market (USD) | Notes |

| Pad‑Mounted (2025) | $24.15B | Dominated by U.S./EU/China demand; three-phase units in utility & commercial networks:contentReference[oaicite:27]{index=27} |

| Power Transformer (2025) | $30.38B | High-voltage units (HVDC, substations); see below |

| Dry‑Type (2024) | $8.1B | Air/solid insulation; see below |

| Distribution (2024) | $21.05B | Overall dist. transformers (includes pad/pole); see below |

Power Transformers

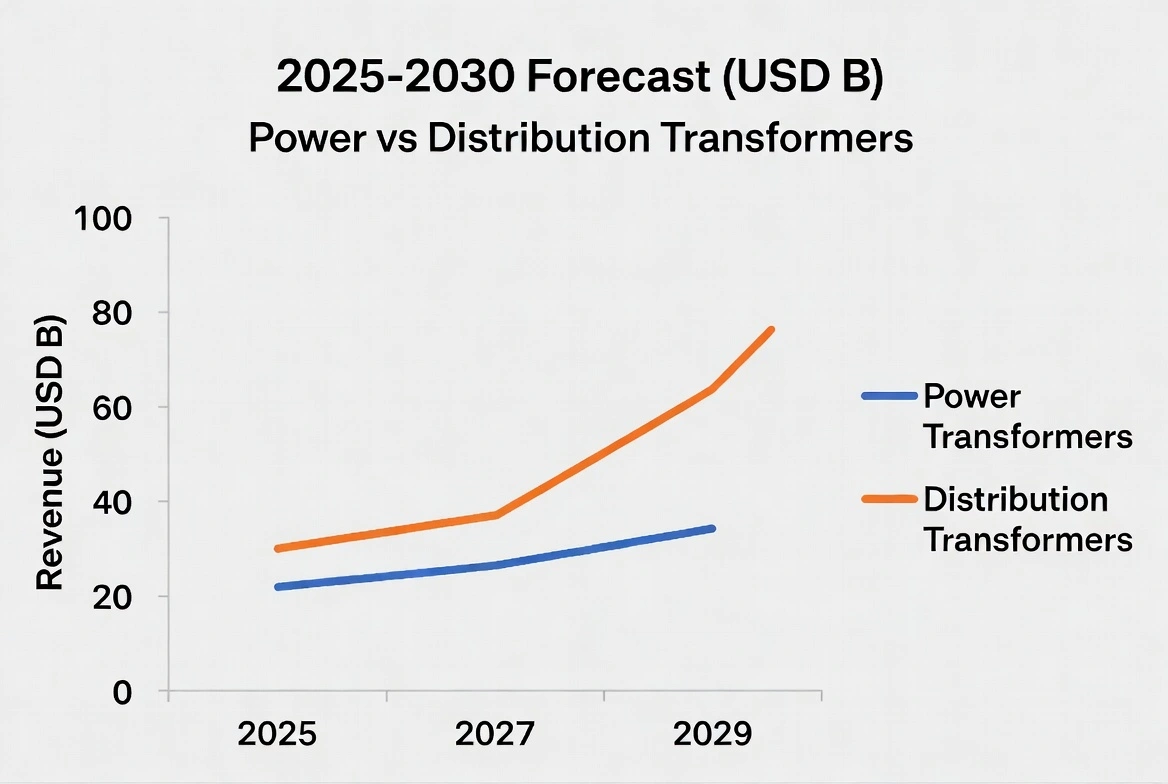

Power transformers step up/down transmission voltages (usually 100–765 kV and above) and are critical for utility grids and large industrial systems. In 2025, the global power transformer market was about $30.38 billion. This includes generator step-up (GSU) and substation transformers. Market growth is driven by global grid reinforcement, renewable power evacuation, and smart‐grid projects. According to MarketsandMarkets, the market is expected to grow at ~6.5% CAGR, reaching $41.62B by 2030. Key factors include rising electricity demand, HVDC adoption, and utility modernization.

Segmentation: By cooling, air-cooled transformers (e.g. cast resin, gas) are the fastest-growing segment, owing to tighter fire/environmental regulations in urban installations. By power rating, medium power units (61–600 MVA) hold the largest share, as these serve sub-transmission networks and industrial grids. The application split is chiefly transmission vs distribution, but exact data are not public. Utilities and bulk power projects form most demand, with growing contributions from renewables (wind/solar farms) requiring high-voltage links.

Regional performance: Asia-Pacific is the fastest-growing region (CAGR ~7–8%), driven by China and India’s massive power grid expansions. Europe and North America also see strong demand from grid upgrades and interconnectors. For example, the European HVDC projects (e.g., NeuConnect UK-Germany cable) are spurring large transformer orders. In 2024-25, the U.S. announced several factory expansions for large power units (e.g., Hitachi’s Virginia plant, Siemens’ North Carolina plant) to meet domestic needs, indicating continued investment. South America's demand is smaller but growing with new hydro and renewables.

Drivers and outlook: The trend toward renewable energy requires more and higher-capacity transformers. The increasing use of HVDC for long-distance transmission (e.g., offshore wind farms) is a notable driver. Grid resilience programs (smart grids, microgrids) also boost demand for robust power transformers. On the flip side, power transformer markets face long lead times and cost inflation: Wood Mackenzie notes that since 2019, large power transformer lead times often exceed 2 years, and prices have risen by ~77%. For 2026, the M&M forecast implies ~$32–33B globally (continuing ~6–7% annual growth). Factors like new renewable projects in Europe/Asia and U.S. infrastructure spending are expected to sustain ~6–7% growth in 2026.

Competition: The power transformer market is led by a few global engineering firms. Major players include ABB Group (Hitachi Energy), Siemens Energy, GE Vernova, Toshiba, Schneider Electric, Mitsubishi Electric, CG (Hitachi), and WEG. Recent contracts and investments illustrate the competitive landscape: e.g., LS Electric (South Korea) secured a $123M U.S. contract for ultra-high-voltage transformers; CG Power won a 765 kV transformer contract in India; Eaton is investing $340M in U.S. three-phase transformer capacity. Power transformers are high-technology, capital-intensive products, so long-standing incumbents dominate. In North America, for instance, ABB, GE/CG, Siemens, and Eaton are the largest suppliers.

Dry‑Type Transformers

Dry‑type transformers (solid or air insulated, no liquid coolant) are increasingly favored in safety‐critical and space‑constrained settings (indoor substations, data centers, schools, hospitals). They eliminate oil-leak and fire risks, meeting stricter environmental/fire codes. The global dry-type market was $8.1 billion in 2024. Transparency Market Research projects a CAGR ~7.3% from 2025–2035, reaching $17.5B by 2035. (DataIntelo estimates ~$4.9B in 2023 and 5.4% CAGR to 2032, which is conservative.) Three-phase units dominate (59% share in 2024), reflecting most installations in large buildings and industrial facilities. By output, low/medium-voltage dry transformers (<35 kV) are the bulk of the market. Industrial and commercial segments are largest, driven by construction in manufacturing, healthcare, and renewable-power operations.

Regional insights: In 2024, North America held the largest revenue share (~30%), due to early adoption in utilities and infrastructure. Europe and APAC are also key markets: stringent EU fire-safety standards and rising data-center construction boost European demand, while rapid industrialization in China/India fuels APAC growth. Latin America is smaller but growing. We estimate 2025 revenues ~8.7–9.0B (from 2024’s $8.1B). APAC is expected to outpace others in CAGR due to new grid builds; North America will grow modestly by retrofitting aging oil transformers.

Applications: Dry transformers serve utilities, infrastructure, and industrial applications. They are common in transport (railways, metros), renewable energy plants (local collection stations), and commercial/IT (data centers, high-tech campuses). A key trend is sensor-equipped smart dry transformers for real-time monitoring, enabling predictive maintenance. Because of their safety, dry units are often installed in urban substations and underground vaults where oil is undesirable.

Forecast (2026): Assuming ~7.3% growth, 2026 dry-transformer revenue will be roughly $9.3–9.5B. Growth drivers include the replacement of old oil-filled units in cities and the continued electrification of sectors like EV charging (dry transformers are used in some charging stations for indoor safety). Leading manufacturers like ABB, Siemens, Eaton, Schneider, and Hammond are expanding dry-transformer capacity. New cast-resin designs (better insulation materials) are improving performance, supporting growth.

Key players: Top companies include Hitachi Energy (ABB), Quality Power (US), Hammond Power Solutions (Canada), Siemens, Eaton, Schneider Electric, GE/CG, and Hyosung. (In dry-type, many power transformer manufacturers also compete.) Industry sources note that ABB and Siemens have each announced larger dry-transformer factories recently. For example, ABB acquired SEAM (asset management services) in 2024 to enhance transformer lifecycle management, signaling a focus on advanced products.

Distribution Transformers

“Distribution transformers” generally refers to all transformers operating at distribution voltages (up to ~35 kV) and serving end-user networks – including pad-mounted, pole-mounted, and small station units. The global distribution transformer market was about $21.05 billion in 2024. (This figure overlaps partially with the pad-mounted figure above; however, market research often treats pad-mounted as a subcategory.) IMARC projects growth to $31.4B by 2033 (CAGR ~4.3%). MarketsandMarkets (2025 base) estimates $21.40B in 2025, rising to $29.57B by 2030 (CAGR ~6.7%). These surveys reflect steady growth as utilities upgrade networks and support new loads.

Regional breakdown: In 2024, Asia-Pacific led with ~45.6% share (driven by China/India T&D expansion). North America’s distribution transformer market was $12.6B in 2024, projected to grow at ~8.8% CAGR (2025–2034) – notably faster than the global average. Europe’s market was ~$7.1B in 2024, with a 9% CAGR forecast (2025–2034). Latin America and the Middle East/Africa are smaller but growing (e.g., Brazil and Mexico invest in rural electrification). South America’s distribution market (e.g,. Brazil, Argentina) is tied to mining and urbanization, with mid-single-digit growth.

Segmentation and drivers: By application, the largest segment is utility distribution networks, serving residential and commercial customers. GM Insights reports that utilities (public power systems) will see ~7–8% CAGR in the U.S., fueled by grid modernization projects. Industrial and residential/commercial end-markets form smaller slices. Drivers include urban population growth, EV charging infrastructure, and renewable integration (e.g., many EV chargers and rooftop panels require local step-down transformers). For instance, increasing EV penetration in Europe (where BEVs hit ~20% in 2024) is expanding transformer demand for charging stations. Regulatory push for energy-efficient equipment (loss minimization) also drives the replacement of old transformers with new units.

Forecast (2026): Assuming ~4–5% growth, global distribution transformer revenue in 2026 will be on the order of $22–23B. U.S. and Europe will grow faster (~6–9% annually in the near term). For example, the GM Insights Europe report expects $7.1B in 2024 to reach $16.9B by 2034 (9% CAGR), implying ~7% growth in 2025–26. In North America, the $12.6B 2024 market (pad, pole, station units combined) is forecast to exceed $18.7B by 2034, a CAGR of ~8.8%. The continued utility focus on reliability and efficiency – e.g., smart grids and distributed generation – will underpin demand. the

Key players: The competitive landscape is similar to that of pad-mounted. Major manufacturers include ABB (Hitachi), CG/GE, Schneider, Siemens, Eaton (Powell), Toshiba, Mitsubishi Electric, Hyosung, Hyundai Electric, Itochu (Nikko), and regional players (e.g., WEG in Brazil, CG in India). GM Insights lists key North American players as ABB, CG Distribution, Eaton, GE, Hitachi, Hyosung, Imefy, Mitsubishi, Ormazabal, Schneider, Siemens, Toshiba, Voltamp. Distribution transformers are lower-voltage products, so many vendors overlap with pad-mounted (as pad units are essentially distribution transformer designs). In 2025–26, manufacturers are introducing features like amorphous cores (to cut no-load losses) and smart monitoring. Recent industry news highlights include ABB acquiring SEAM Group (asset-management services for transformers), and utilities ordering advanced ‘smart’ distribution transformers from GE and others (not detailed in public sources).

Outlook and Charts

Overall, all four transformer segments are on growth trajectories in 2026, albeit at varying rates. Pad-mounted and distribution units benefit from rapid urbanization and renewables (CAGR ~6–9%), power transformers grow steadily (~6–7%), and dry-type units grow fastest (~7%+). Drivers include unprecedented T&D build-outs, replacement of aging equipment, and new electricity-intensive sectors (EVs, data centers). Constraints remain: long lead times (often >18 months for large units), higher raw material costs (steel, copper), and supply-chain bottlenecks.

While an exact 2026 forecast depends on regional factors, a summary projection is:

- Pad‑Mounted: ~$26–27B (USD) by end-2026 (c. +6–7% vs 2025).

- Power: ~$32–33B by end-2026 (+6–7% vs 2025).

- Dry‑Type: ~$9.3–9.5B by end-2026 (~+7% vs 2024).

- Distribution: ~$22–23B by end-2026 (+4–5% vs 2025).

Each segment’s forecast assumes continuation of current drivers (grid investments, renewables, safety regulations) and does not account for unforeseen supply shocks. Industry sources uniformly stress the ongoing “transformer shortage” in 2025–26; mitigating this through domestic capacity expansion is a key theme.

Related Articles

Related Products

35kV Concentric Neutral Underground Power Cable

The 35 kV Concentric Neutral Power Cable is a high-performance medium-voltage underground cable designed for primary distribution systems. It features a stranded conductor, semi-conducting shields, tree-retardant TR-XLPE or EPR insulation, helically applied bare copper concentric neutral wires, and a sunlight-resistant LLDPE jacket. This construction provides excellent electrical performance, superior resistance to water treeing, and robust mechanical protection suitable for direct burial or duct installations. Available in various conductor sizes and insulation levels, the cable ensures safe and efficient power delivery. Manufactured to the latest ICEA S-94-649 and AEIC CS8 standards, the 35 kV Concentric Neutral Power Cable undergoes extensive quality testing to deliver consistent low dielectric loss and long service life in demanding underground environments.2Y-high-voltage-power-cable-2.webp)

2XS(FL)2Y HDPE High Voltage 36/60 (72.5) kV Power Cable

The 2XS(FL)2Y HDPE High Voltage 36/60 (72.5) kV Power Cable is a high-performance single-core copper conductor cable designed for medium-to-high voltage power transmission. It features XLPE insulation, extruded semi-conductive conductor and insulation screens, and semi-conductive water-swellable tapes for longitudinal water blocking. A longitudinally applied aluminium tape moisture barrier coated with PE copolymer ensures superior moisture resistance and mechanical protection. The HDPE oversheath provides outstanding abrasion, chemical, and environmental resistance, making it suitable for direct burial, underwater, outdoor, indoor, and duct installations. Manufactured in compliance with IEC 60840, this cable guarantees reliable long-term electrical performance in demanding environments such as power stations, industrial plants, and distribution networks.

2/0 Cavolinia Aluminum Conductor Triplex Overhead Service Drop Cable

The 2/0 Cavolinia Triplex Service Drop Cable is a reliable overhead cable for secondary power distribution to residential service entrances. Featuring two 2/0 AWG aluminum phase conductors and one neutral messenger (7-strand) insulated with XLPE or PE and assembled in triplex configuration, it provides excellent mechanical strength and weather resistance. Compliant with ASTM B-230, B-231, ICEA S-76-474, and ANSI/ICEA standards, this cable supports 600V applications with high UV, moisture, and abrasion protection. The self-supporting messenger reduces sag and simplifies installation over medium spans. The 2/0 Cavolinia Triplex Service Drop Cable ensures low power losses, high current capacity, and long service life in harsh outdoor conditions. Lightweight and flexible, it is widely used for two-phase service drops with neutral in urban, suburban, and rural areas requiring safe, cost-effective aerial connections from utility poles to homes.

2 Palomino Aluminum Conductor Quadruplex Overhead Service Drop Cable

2 Palomino Aluminum Conductor Quadruplex Overhead Service Drop Cable is designed for delivering 3-phase power from pole-mounted transformers directly to the user's service entrance. Built with three 2 AWG aluminum phase conductors and one neutral messenger (7-strand) insulated with polyethylene or XLPE and formed into a quadruplex assembly, it meets ASTM and ICEA requirements for 600V service. The tough insulation offers outstanding protection against UV rays, moisture, tree contact, and abrasion. Self-supporting messenger design ensures easy pulling and reduced sag during installation. The 2 Palomino Quadruplex Service Drop Cable supports efficient power transfer with low voltage drop and high durability in extreme temperatures. Popular for its lightweight construction and reduced installation time, it is the choice for electricians and utilities. Widely deployed in housing developments, commercial services, and temporary power setups, this cable ensures safe, long-lasting overhead connections from distribution transformers to customer service entrances worldwide.

4 Whippet Aluminum Conductor Duplex Overhead Service Drop Cable

The 4 Whippet Duplex Service Drop Cable is a durable overhead cable for secondary power distribution to residential service entrances. Featuring two 4 AWG aluminum conductors (phase and neutral, 7-strand) insulated with XLPE or PE and assembled in duplex configuration, it provides excellent weather resistance and mechanical strength. Compliant with ASTM B-230, B-231, ICEA S-76-474, and ANSI/ICEA standards, this cable supports 600V applications with high UV, moisture, and abrasion protection. The self-supporting design simplifies installation with reduced sag over spans up to 100 feet. The 4 Whippet Duplex Service Drop Cable ensures low power losses, reliable performance in harsh outdoor conditions, and long service life. Lightweight and flexible, it is widely used for single-phase service drops in urban, suburban, and rural areas requiring safe, cost-effective aerial connections from utility poles to homes.

75kVA Completely self-protected(CSP) Single Phase Pole Mounted Transformer

NPC ELECTRIC, the production of a 75kVA Completely Self-Protected (CSP) Single Phase Pole Mounted Transformer is a high-efficiency, reliable solution for single-phase power distribution in residential, commercial, and small industrial applications. Equipped with built-in protection features such as overload, short-circuit, and over-voltage protection, it ensures automatic disconnection during fault conditions to prevent damage to the system. Its pole-mounted design saves space and is ideal for installation in both urban and rural environments. The transformer operates with minimal energy loss, ensuring high efficiency and long-term performance, while its durable construction makes it resistant to harsh weather conditions, ensuring a reliable and safe power supply over time.

(N)TSCGECEWOU 3.6/6kV and 6/10kV ATB Cable

The (N)TSCGECEWOU 3.6/6kV and 6/10kV ATB Cable is a flexible, heavy-duty medium-voltage trailing/reeling cable with anti-torsion braid (ATB) for superior torsional stability in extreme mining conditions. It features class 5 finely stranded tinned copper phase conductors for flexibility and corrosion resistance, semi-conductive conductor and insulation screens, EPR insulation for high dielectric strength and 90°C rating, copper wire braid screen for EMI/grounding, control conductors, monitoring conductor (ÜL), anti-torsion polyester braid for reduced twisting under dynamic loads, and a tough rubber outer sheath resistant to oil, flame, abrasion, and mechanical stress. Compliant with DIN VDE 0250, it handles high tensile forces, fast reeling, and tight bends while providing EMC protection. The (N)TSCGECEWOU ATB ensures safe, reliable MV power to mobile equipment like draglines, shovels, and tunnel boring machines in harsh opencast/underground environments.

NA2XSY Medium Voltage Power Cable(6/10kV, 12/20kV, 18/30kV)

NA2XSY are medium voltage power cables with aluminum conductors and XLPE insulation, designed according to IEC 60502-2 standards. Constructed with aluminium conductors, thermosetting XLPE insulation, metallic screen (copper tape or wires), and tough PVC outer sheath, it meets IEC 60502-2 requirements. The screen ensures electromagnetic compatibility and fault protection. Low tan delta, high breakdown strength, and excellent thermal endurance minimize losses and support overloads. PVC sheath provides reliable mechanical and moisture protection for fixed installations. Optional longitudinal water-blocking improves performance in damp areas. Flame-retardant and easy to install, the NA2XSY Medium Voltage Power Cable is favored for power grids, manufacturing plants, commercial developments, and renewable energy sites demanding cost-efficient single-core medium voltage cabling with proven durability and performance in buried or tray installations worldwide.

Instrumentation Cables—XLPE Insulated, Overall Screened, Wire Armoured PVC Sheathed Cables(CU/XLPE/OSCR/SWA/PVC)

Engineered for thermal resilience and electromagnetic shielding, the Instrumentation Cables—XLPE Insulated, Overall Screened, Wire Armoured PVC Sheathed Cables (CU/XLPE/OSCR/SWA/PVC) excel in high-temperature environments. Stranded copper conductors ensure low resistance and flexibility, with XLPE insulation providing 90°C continuous rating and 250°C short-circuit tolerance. Overall screening via aluminum/polyester tape and drain wire mitigates EMI/RFI, preserving signal quality. SWA armour protects against mechanical damage, while PVC sheath adds flame resistance and waterproofing. Meeting BS EN 50288-7 and BS EN 50288-1 standards, these multi-pair cables transmit analogue/digital signals with low capacitance in demanding circuits. Suitable for ducts, trays, direct burial, or outdoor exposures, they boost system integrity and reduce interruptions in heat-intensive areas. With enhanced dielectric properties and attenuation control, this CU/XLPE/OSCR/SWA/PVC offers dependable, maintenance-reducing solutions for professionals in petrochemical, power, and industrial sectors.

(N)TSCGEWOU 3.6/6kV, 6/10kV, 8.7/15kV and 12/20kV ATB Cable

The (N)TSCGEWOU 3.6/6kV, 6/10kV, 8.7/15kV, and 12/20kV ATB Cable is a medium voltage flexible power cable designed in compliance with VDE 0250 standards. It features Class 5 tinned copper conductors, EPR rubber insulation, semi-conductive layers, halogen-free flame-retardant rubber sheath, and an earth detection conductor. The ATB construction ensures superior mechanical strength, oil resistance, abrasion resistance, and flame retardancy, making it ideal for open-pit mining, tunneling, and other heavy-duty mobile equipment applications under extreme mechanical stress. It includes tinned class 5 copper phase conductors, semi-conductive screens, EPR insulation for reliable dielectric and thermal performance (90°C rating), copper braid screen, control conductors, monitoring conductor (ÜL), anti-torsion braid to reduce twisting under load, and a robust rubber sheath resistant to oils, flames, abrasion, and mechanical damage.

320 kV High Voltage Power Transformer

NPC Electric 320 kV High Voltage Power Transformer is engineered for ultra-high-voltage transmission networks where reliability, efficiency, and operational safety are critical. Designed to handle extreme electrical stress, this transformer supports stable power transfer across long-distance transmission lines and major grid interconnection points. Its oil-immersed insulation system provides superior dielectric strength and efficient heat dissipation, ensuring consistent performance under continuous high-load conditions. Advanced core optimization reduces magnetic losses, while precision winding design enhances voltage regulation and system stability. The transformer structure is built to withstand thermal expansion, mechanical forces, and short-circuit events, making it suitable for demanding grid environments. With long service life, low maintenance requirements, and high operational efficiency, the 320 kV power transformer is an ideal solution for modern high-voltage substations and large-scale energy infrastructure projects.

630kVA Single Phase Pad Mounted Transformer

Elevate your underground power distribution with the robust 630kVA Single Phase Pad Mounted Transformer, specifically designed for high-demand residential and commercial loop-feed networks. This oil-immersed, single-phase unit incorporates premium electrical steel laminations and heavy-duty windings to minimize energy losses and provide outstanding thermal performance under continuous loads. Meeting ANSI C57.12.38 and IEEE C57.12.90 standards, this 630kVA padmount transformer delivers precise voltage transformation from primary levels up to 34.5kV to common secondary voltages like 120/240V or 277/480V, supporting extended overloads and long-term reliability in densely populated areas.

250kVA Three Phase Pad Mounted Transformer

The 250kVA Three Phase Pad Mounted Transformer is a compact, liquid-immersed, self-cooled (ONAN) distribution transformer optimized for efficient, underground power delivery in residential, light commercial, and small industrial applications. Fully compliant with IEEE C57.12.34, ANSI C57.12.00, DOE 2016 efficiency standards, and UL-listed, this compartmental-type unit features dead-front 200A high-voltage bushing wells (loadbreak inserts), radial or loop feed options, and a sealed tank using non-PCB mineral oil or FR3 natural ester fluid for improved fire safety and environmental performance.

Type 210 Flexible Rubber Mining Cable

The Type 210 Flexible Rubber Mining Cable is a 1.1kV medium-voltage cable engineered for mining handheld drills and boring machines. It features flexible stranded tinned annealed copper conductors, EPR insulation, and a composite copper/polyester screen for improved electrical shielding. The heavy-duty PCP sheath offers oil resistance, abrasion protection, and flame retardancy, ensuring durability in harsh underground conditions. Compliant with AS/NZS 2802 and related standards, this cable delivers long-lasting performance in demanding environments requiring high flexibility and mechanical strength.

11/0.4kV Dry Type Transformer | Indoor Power Transformer

Discover the reliable 11/0.4kV Dry Type Transformer | Indoor Power Transformer, a safe, oil-free solution designed for efficient medium-to-low voltage conversion in indoor electrical installations. This three-phase dry-type transformer (typically cast resin or vacuum pressure impregnated) features premium low-loss silicon steel cores and high-conductivity copper windings, achieving superior energy efficiency often exceeding 98% and complying with IEC 60076-11 standards. The epoxy resin encapsulation provides excellent moisture resistance, fire self-extinguishing properties (F1 class), minimal partial discharge (<10pC), and robust short-circuit withstand capability. With natural air (AN) cooling and optional forced air (AF) upgrades, it offers low noise operation, Class F/H insulation, and maintenance-free performance in demanding environments. Ideal for step-down from 11kV primary (with ±2×2.5% or wider off-circuit taps) to 0.4kV secondary (Dyn11 vector group standard), this indoor power transformer supports capacities from 100kVA to several MVA, delivering stable, eco-friendly power distribution without oil-related risks.Welcome your inquiry

Honesty, Integrity, Frugality, Activeness and Passion